now loading...

Global dividends reached a new annual record of US$2.09 trillion in 2025, up 7.0% year-on-year on a topline basis, according to a recent report.

Core dividend growth was 6.0% after adjusting for exchange rates, one-off payments and calendar factors. At the company level, median dividend growth was 5.8%, finds the latest Dividend Watch report, part of the Capital Group’s Global Equity Study.

The year ended on a high note, with payouts hitting a Q4 record of US$428 billion, the report notes, underlining the resilience of dividend growth. Q4 topline and core growth were 6.5% and 5.9% respectively.

“Dividend growth reached record levels in 2025 supported by robust earnings and broad-based strength across regions and sectors, with only limited pockets of weakness,” says Alexandra Haggard, Capital’s head of asset class services for Europe and Asia-Pacific. “Looking at 2026, there are many encouraging signs for the year ahead with global equity markets broadening, more companies driving returns and dividends well supported by the earnings outlook.”

Sectors

Financials were the key driver of dividend growth in 2025, the report points out, with insurance and general financials posting rapid increases in payouts, up 12.5% and 16.8% respectively.

Technology delivered the second-fastest core growth led by software and IT services, which recorded a 13.0% core increase. Software dividends were broadly comparable with the auto sector’s a decade ago, but in 2025, they were 45% larger at a record US$64.1 billion.

Pharmaceuticals, utilities, media and machinery – particularly aerospace and defence – were also major contributors. Only mining, car makers and oil, gas and energy saw lower payouts, reflecting a combination of weaker profits in cyclical industries.

Markets

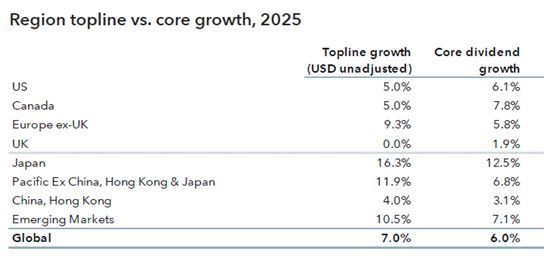

Geographically, growth was broadly spread with record payouts in 30 of the 46 markets or territories in the Capital Group index, the report shares, including the US, Japan, Canada, Singapore, Hong Kong, Taiwan and most of Europe. The weak US dollar boosted the number of dollar record breakers.

Japan led the way, with payouts rising twice as fast ( +12.5% ) as the global average, reflecting a greater focus on governance and shareholder remuneration, while the US, emerging markets, Canada and Europe all saw core growth of around 6% to 7% for the year.

US payout growth has normalized after being boosted by large new technology payers in 2024, while in Europe, there were broad-based increases in most countries and sectors with median dividend growth of 6.8%, ahead of the global average.

Australia, with its heavy exposure to resources and slower-growing banks, was a notable weak spot. The UK lagged due to mining and telecoms, while in China, pressure on corporate profits transmitted mechanically to dividends via fixed payout ratios.

Hong Kong, China

In Hong Kong, payouts just exceeded their previous 2017 high, the report highlights, rising 8.5% on a core basis to US$25.5 billion. Core Q4 growth was 4.3%, with financials delivering around one third of the growth.

The dividend picture in China was significantly muddied by a major calendar shift that has seen more and more Chinese companies breaking their traditional single annual payment into two smaller ones.

This factor alone added close to US$4 billion to the topline total during the year, roughly offsetting lower special dividends in the topline growth rate. Core growth in China was just 2.3% during the year ( and 2.8% in Q4 ).

Singapore

In 2025, Singapore recorded rapid topline growth of 19.3%, the report details, driven primarily by large special dividends from the banking sector, as well as significant increases in normal dividends.

These gains were sufficient to offset a small number of notable cuts. Exchange rates also boosted the topline figure. With much of the increase attributed to one-off dividends during the year, the 2025 core growth rate was a modest 2.1%.

However, since the banking sector’s special dividends reflected strong trading and capital positions, the topline growth arguably provides a fairer representation of the year’s performance.

The total payouts reached US$18.7 billion in 2025, the largest since 2021, when there were some large catch-up payments after 2020’s pandemic-related cuts.

Source: Capital Group Global Equity Study: Dividend Watch Edition 3

2026

Projection for 2026 is 5.4% topline payout growth, the report highlights, a new record of US$2.20 trillion, equivalent to core growth of 5.7%.

“In an environment dominated by geopolitical uncertainty, tariff tensions and alternating phases of volatility, companies that pay dividends and show they can grow them sustainably over time offer stability to portfolios,” adds Toby Chan, Capital’s head of client group for Hong Kong and Greater China. “For investors in Singapore, Hong Kong and China, dividends can continue to provide a dependable source of income and resilience across market conditions.”